In March, four major banks failed. Brian O’Boyle looks at why this happened and assesses the risk of further instability in the global banking system.

Warren Buffet famously quipped that “it is only when the tide goes out that we find out who has been swimming naked”. Chair of the world’s most successful investment firm, Buffet understands the confidence trick at the heart of modern finance. When finance is cheap, it can be difficult to separate firms that have strong fundamentals from those surviving on cheap credit. But when interest rates increase, weaker banks come under pressure, as their liquidity (sources of cash) dries up and investors desert them.

In March 2023, the tide went out on four such banks in quick succession. US regulators closed three of them, including Silicon Valley Bank (SVB) and Signature Bank – the second and third largest bank failures in US history. In Europe, Credit Suisse was merged with UBS as a government injection of $50 billion failed to convince investors that it could survive. Silicon Valley Bank was the 16th largest bank in the US. Credit Suisse was one of Europe’s 12 major investment firms and although it had been in trouble for months, it was the collapse of SVB that pushed it over the edge. Investors suddenly judged that Credit Suisse may not be too big to fail, leaving regulators panicking that other banks could soon follow suit.

So far this hasn’t happened, but with interest rates higher than they have been for 15 years, banks are now operating in a more challenging financial environment. We will explain this further below, but first it is useful to understand how banks make their money.

Fractional Reserve Banking

Successful banks rely on two main sources of finance – investment and deposits. Investment occurs when the owners of capital are willing to lend it on to financial organisations. This allows the recipients to make their own investment decisions and/or hold the capital to use it later. It also feeds into higher share prices for the company and higher bonuses for senior executives. Deposits are placed with banks by those with savings. Here the motivation is a return for the saver, while for the bank, deposits are the foundation for making loans.

Banks operate a system known as Fractional Reserves. By law, a bank must keep a fraction (say 10%) of their deposits in reserve, meaning they can’t lend this portion out. If a bank has €100 in deposits for example, and they are required to hold 10% of their loan book in reserve, they can make loans of €900 from this €100 deposit. This credit allows the borrower to acquire goods and services today in exchange for paying for them gradually over time. Banks have thousands of loans with different maturities, meaning they can cover the cost of the credit they give to borrowers today (their liabilities) with the money gradually flowing in from previous borrowers (their assets). Banks charge and receive interest for these transactions and the difference between the amount they must give their depositors (of the €100) and receive from their borrowers (of the €900) is the basis of their profits.

This makes the deposit base extremely important. It also makes banks unusually vulnerable to sentiment and crisis. To make profits, banks must have loan books many multiples of the amount of capital they hold in reserve. But reserves don’t make them any profits, so banks always hold as little reserves as possible, leveraging their deposit base as much as they can. This makes for risky business, as default is always a possibility, and the more loans are made against a given deposit base the riskier the whole process becomes. If borrowers meet their obligations, the bank makes profits, but if they don’t, the bank still owes returns to its investors and interest to its depositors. If either of these groups gets spooked, it can cause a run on the bank as investors and depositors look for their money back. This can only be stopped if the bank gets enough money to re-establish confidence – often from taxpayer bailouts or selling off its assets, but also from other banks, investors, or depositors.

Higher Interest Rates

Now think about the wider economic environment. In 2008, the global financial system basically disintegrated as banks were squeezing borrowers and capitalists were squeezing wages. Millions found themselves unable to service their debts and a financial catastrophe was only averted through taxpayer bailouts costing trillions of dollars. In the intervening period, the financial system was kept alive on a diet of extremely cheap money known as quantitative easing (printing money). Meanwhile, the banks were forced to increase their reserves and make investments judged safer by the markets. This often meant a preference for government bonds that contained a lower risk of default. Although lower interest rates made it hard for banks to make high returns, the cost of their own borrowing was also low, and they got all manner of advantages from capitalist institutions. The European Central Bank made sure banks made profits for example, by refusing to lend to national states directly. The US state granted $700 billion to the financial system in the first months of the crisis followed by trillions more in quantitative easing – often used to purchase US Treasury Bonds.

The price of these bonds has an inverse relationship with the interest rate, moreover, meaning that when interest rates were artificially low, bond prices were relatively high. To explain this, imagine you own a bond worth $1,000 that is due to be repaid by the US state in 2025. In the meantime, you receive 3% interest annually for allowing the US government to use your money ($30 annually). If the official interest rate is 1%, this investment looks good, but if the official rate goes up to 5% then your rate of 3% is no longer attractive. To get a 5% return you will need to sell the bond and invest in the bank, but no one will be willing to pay €1,000 for a bond that will only give them a 3% return. Instead, they will only be willing to pay $600 for an asset that will allow them the same 5% return ($30 annually) they can get off the bank. The bond price has fallen as interest rates have risen. In the last 12 months, interest rates in the US have been increased nine times from a base rate of 0.25% to a base rate of 5%. In Europe, the ECB has increased interest rates 6 times from a base rate of 0% to a base rate of 3.5%. The aim is to dampen post-Covid inflation but the consequences for financial institutions have been destabilising.

The most obvious consequence has been losses on the value of bonds held by the banks. A recent article in the Financial Times estimates that US banks are sitting on losses of $620 billion on bonds that will have to be marked down if they need to be sold. Stronger lenders can sit on their bonds until their maturity date, but weaker ones may not have this luxury. One reason SVB failed was that it was forced to sell bonds at a loss as depositors withdrew their liquidity. This was partly because many of them are in the technology sector and needed the cash and partly because of a drop in market confidence in the lender itself. A related consequence of higher interest rates has been deposits moving from banks with less market confidence for those with more. Michael Roberts estimates that around $500 billion has been withdrawn from smaller US banks since the collapse of SVB with about 50% of this going to bigger – better capitalised – banks, and the rest looking for higher yields in money market funds. These are vehicles that offer higher returns by stripping out normal banking services to their customers. They cut costs to offer higher rates to depositors and use their money to invest in slightly higher risk activities.

In the Eurozone a similar pattern has been unfolding as depositors withdrew €215 billion since inflation began with €71 billion withdrawn in March alone – the highest monthly total since records began in 1997. Overall, this still isn’t a lot of money (about 1.5% of total deposits), but less well capitalised banks may find themselves in trouble causing contagion – a spread of panic – for other lenders.

The long period of cheap money also meant banks wrote an unusually high volume of their loans with fixed interest rates. They expected the era of cheap money to continue indefinitely and now face two problems as a result (1) many of their loans have fixed interest rates which lose money for the lender (2) increasing the cost of variable rate loans increases the risk of default by some borrowers.

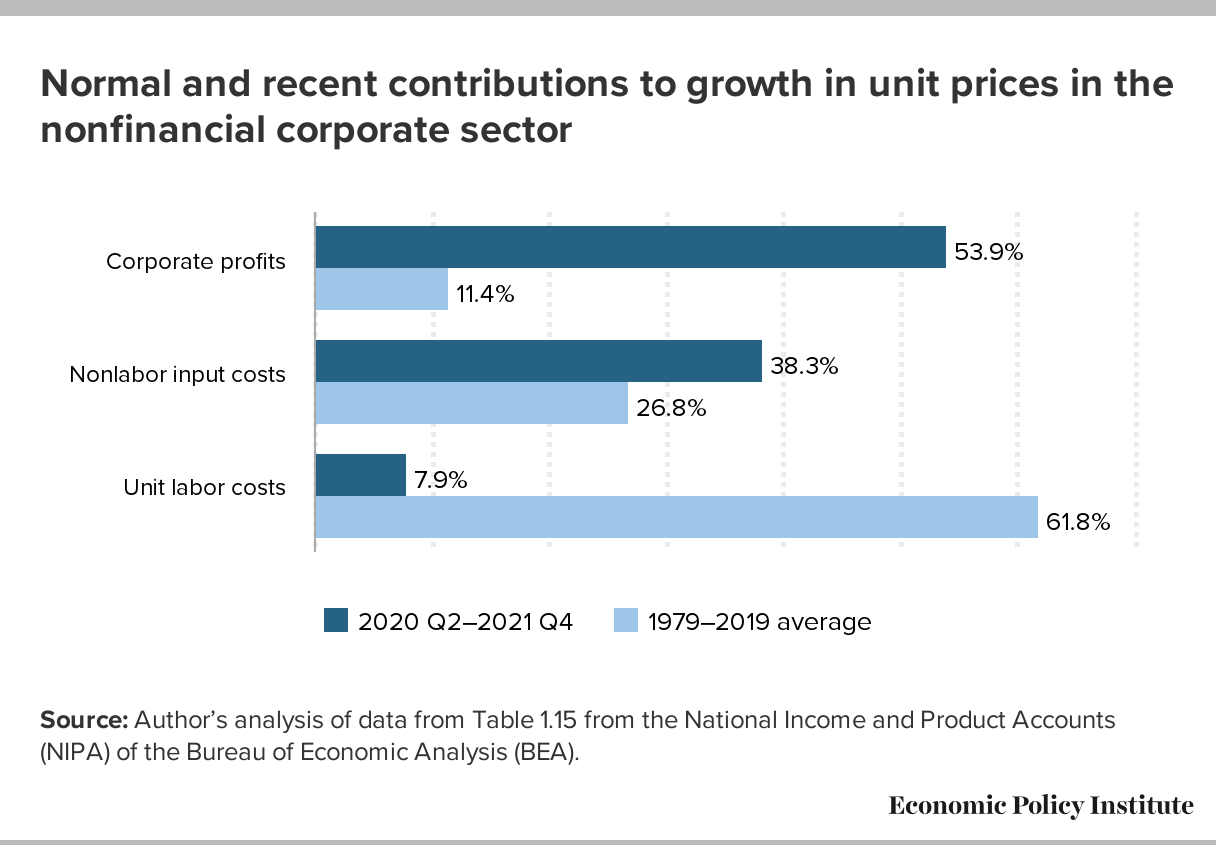

In this context, it is worth remembering that many homeowners are already being stretched by the sharpest increase on the cost of living for 40 years. It is also worth remembering that for all the profit gouging that has characterised the last 12 months, one in five companies in the OECD are now defined as Zombie companies. In other words, companies that have historically been unable to pay their way and persist by rolling over short-term loans at low interest rates.The Economic Policy Institute has estimated that profit gouging is the major driver of the current inflation, as businesses use the cover of Covid 19 to ramp their prices way ahead of their increased costs. For some companies this can be explained solely by the logic of profit, but for others it may have been a welcome respite from a long period of stagnation. The graphic below captures the dynamics of the recent period of higher prices.

Zombie companies may soon find themselves squeezed for three different reasons. Most obviously they will have to find more money to meet their financial obligations as interest rates increase, but they may also struggle to source customers with less disposable income around at the same time as their own lenders find safer options to lend out money.

All of this means that the current period of higher interests has the potential to set off a rolling wave of bankruptcies and layoffs with knock on effects for bankers and the wider economy. A recent article in the Harvard Business Review puts it this way: “With economic conditions changing rapidly…these firms might start dying off. Zombies feast on cheap credit, and rising interest rates mean that’s suddenly in short supply. Some say zombies’ time is running short. The end result could be a prolonged stretch of bankruptcies unlike any in recent memory.”

Whether this occurs or not, claims by mainstream commentators that the recent collapses are not systematic seem wide of the mark. Thus far, the scale of the crisis is not comparable with the disaster of 2008, but with interest rates higher than they’ve been for a generation, financial instability is likely to persist for smaller lenders and those with weaker balance sheets – and if they do get into trouble, taxpayers will be forced to pick up the tab. Swiss taxpayers have already had to fork out $13,500 each to clear up the mess around Credit Suisse while for Irish taxpayers the collapse of 2008 is still being felt as they each fork out €21,500 to failed banks in the state. With this in mind it is worth reiterating the case for a socialised banking system that would replace the search for short term yield with longer term goals for people and the planet.

The Real Costs of Private Banking

According to mainstream textbooks, private banks fulfil three main purposes in the capitalist economy

- By administering a sophisticated payments system, they facilitate a sophisticated division of labour as people specialise in production and trade with each other using money as a universal means of exchange.

- They create and manage the credit system allowing people to purchase goods and services when they desire them. This allows capital to find instant customers and consumers to find instant gratification.

- They recycle society’s unused surpluses – matching savers with investors so that economic investment can continue, and the economy will grow.

A sophisticated payments system is required to have a modern economy, but this does not have to be controlled by unelected financiers who gain incredible political power through their control of the payments system. When Irish workers were being hammered with austerity, for example, they were told that a financial bomb would go off in the Irish financial system if the government refused to pay wealthy.

Enda Kenny used similar rhetoric when threatening workers that the army might have to ration their access to ATMs, while in Greece, it was control of the Greek financial system by the European Central Bank that ultimately hobbled Syriza’s progressive agenda, even if their own reformist politics were also a factor. The point is that allowing unelected financiers to control our payments system, also affords them untold influence over the rest of our lives. Private control of the financial system is incompatible with democratic control of society at large – a point constantly underlined by the ECB’s control of the Monetary Union. A socialist banking system would maintain a universal means of exchange without the class logic that currently underpins it.

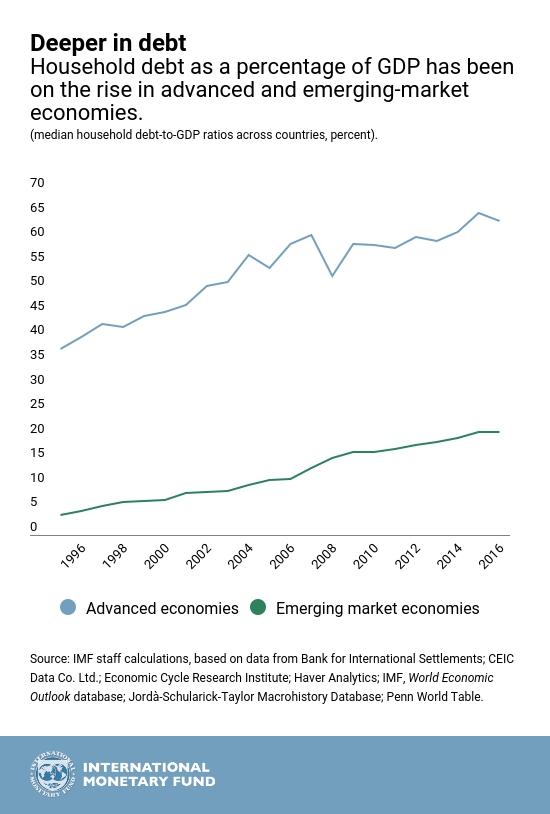

The second function is also important, but it misses two central problems that influence credit creation in the neoliberal era. The first is the massive increase in household indebtedness as families are forced to hand ever more of their earnings to bankers and financiers. These are not merely technical issues of credit creation – they are embedded in a system of deep injustice, as working people are being forced to borrow more and more just to make ends meet. A point illustrated by the IMF graphic below.

The second problem with credit creation is the deep instability caused by capitalist banks in search of yield. Today much of the credit system is in shadow banks outside the regulatory system, but inside the capitalist system itself. This is one reason why there have been 147 major banking crises since 1970 versus less than 10 in the period from 1945-1970, as financiers engage in ever riskier ways to make a profit.

Each of these crises creates misery for the working people forced to pick up the tab, but it also creates problems with moral hazard. This refers to changes in behaviour by those who take risks but are shielded from any negative consequences. Right wing economists trot out the dangers of moral hazard when criticising debt forgiveness for ordinary borrowers, but they have no problem with it when governments repeatedly bail-out financial elites. The biggest banks know they are too important to fail. They also operate in a highly competitive environment driving the kinds of risky behaviour that crashed the economy in 2008.

Ultimately the credit system reflects the power of capital over labour – a power that would no longer be operative in a socialist banking model. Whether this meant credit itself would be a thing of the past is unclear but what is clear is that credit would not be used to systematically extract value from working people.

The final function of the financial system – that of matching savers to borrowers – is also problematic when run under the logic of profit. It is true that major investment houses re-cycle funds into their most profitable avenues, but they are incapable of doing this in ways that facilitate social justice and environmental sustainability. According to Dilan Riley, “what the planet and humanity need is massive investment in low-return, low productivity activities -care, education and environmental restoration.

Capital is incapable of doing this. It seeks ‘value’ which these sectors struggle to produce. The underlying reason is obvious: neither health, nor culture, nor the umwelt function very well as commodities. The endless search for yield has caused the climate crisis so it won’t be capable of solving it. It has also caused a world in which the richest eight men have more wealth than the bottom fifty percent combined. Finance capital is at the very heart of the neoliberal system. We need to make human need the centre of the system that replaces it.